Making Sense of Private Credit Markets Amidst the Recent Selloff

Private credit markets are experiencing a clear division between managers who prioritize disciplined credit underwriting and those focused on capital deployment, leading to varied fund performance and market repricing of risk.

The following summarizes the main points covered in this article:

- Performance divergence in private credit products: Some private credit funds are underperforming due to lax underwriting, covenant erosion, excessive leverage, and declining pricing power, reflecting capital deployment rather than quality investment opportunities.

- The BDC structure is not the problem; credit discipline is the culprit: Publicly traded Business Development Companies (BDCs) are often blamed for poor returns, but the real issue lies in credit discipline, not the fund structure itself.

- The Difference Between Beta and Alpha Managers in Private Credit is revealing itself: Beta managers rely on capital deployment, leverage, and floating rate exposure, often accepting higher risk to maintain returns, while Alpha managers focus on underwriting skill, strong covenants, senior secured positions, scale discipline and selectivity to generate returns.

- Structural substitution risk: To maintain yields, many managers accept higher borrower leverage, weaker covenants, increased fund leverage, refinancing risks, and reduced lender control, shifting risk to creditors without adequate compensation.

- Markets are repricing structural substitution risk: Despite low default rates and contained non-accruals, markets are discounting liquidity-sensitive, covenant-lite, and leveraged strategies ahead of realized losses, reflecting concerns over deteriorating credit discipline.

- Scale pressures impact credit quality: Large managers face operational challenges deploying capital in lower-middle-market bespoke lending, leading to migration toward larger deals, more competition, and financial engineering, which diminishes credit quality.

- Characteristics of true private credit alpha: Alpha is demonstrated through first-lien senior secured positions, enforceable maintenance covenants, sponsor equity alignment, appropriate use of funds, and the capacity to refuse poor deals, which protect against structural decay.

- Outlook and discipline emphasis: The private credit market is undergoing a sorting process favoring discipline, selectivity, and structure over scale and deployment, positioning informed investors advantageously for the next cycle.

Market Dynamics in Private Credit

In 2023, market observers—including institutional allocators and credit analysts—noted concerns that certain private credit funds were lowering credit standards to achieve scale. Those concerns are now manifesting in market performance.

Disclaimer: Past market observations do not guarantee future analytical accuracy or investment results. This analysis represents the author's perspective based on publicly available market data.

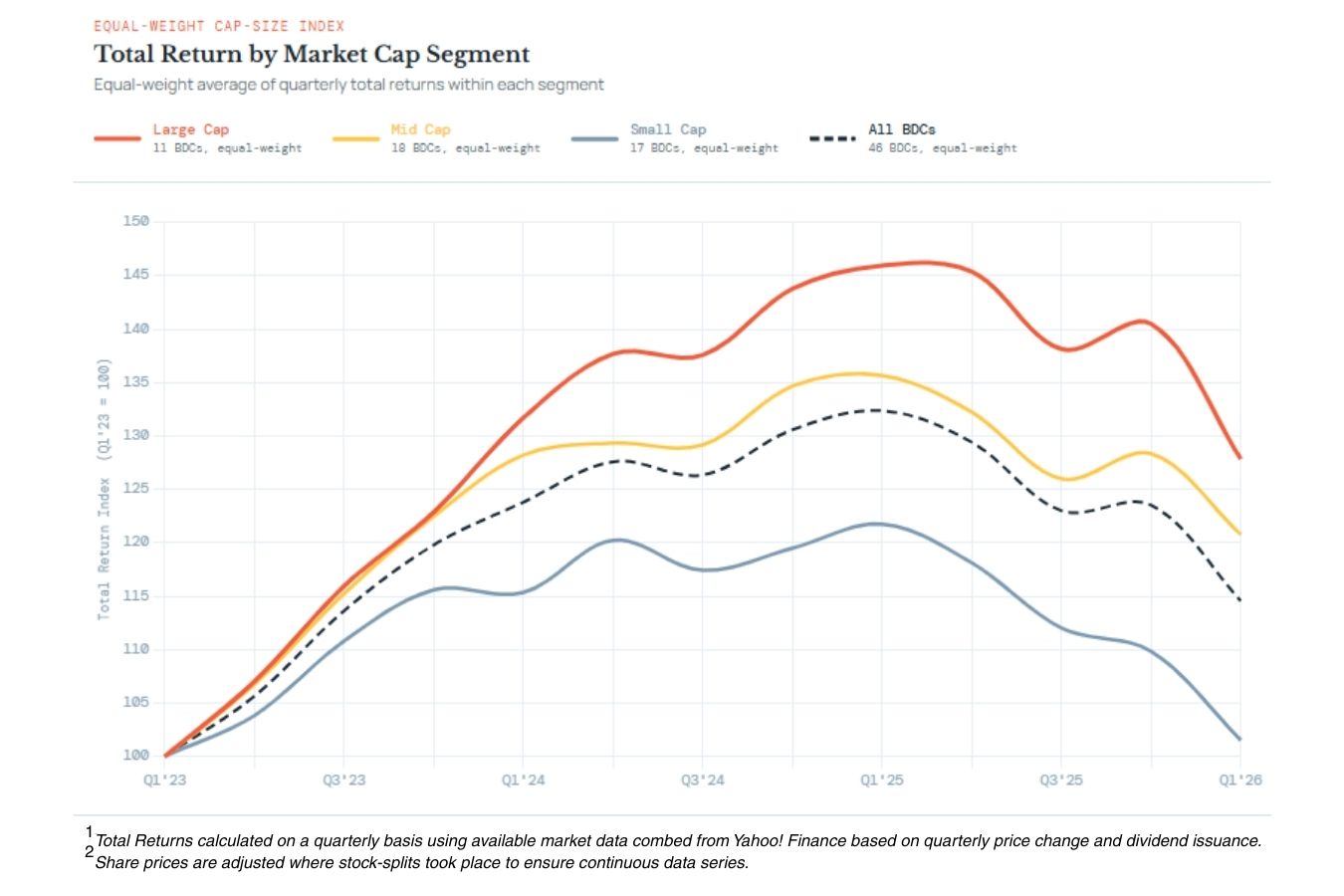

The chart below shows a snapshot of Private Credit BDC performance over the last 2 years:

To be clear, performance is not uniformly poor across private credit funds, but there is a clear pattern exhibited amongst the funds that are underperforming.

Those funds exhibit:

- Lax underwriting

- Increased acceptance of subordination to achieve yield

- Covenant erosion

- Excessive use of fund leverage

- Declining pricing power (in terms of interest rates charged) for 1st Lien positions

- Participation in larger and larger deals.

Said differently, they are deploying capital for the sake of deployment, not because they have a plethora of great underwriting opportunities.

What we are witnessing today is not a collapse of private credit as an asset class, nor a structural failure of fund vehicles like BDCs. Instead, we are seeing a long-anticipated bifurcation — between managers who generate returns through true credit skill (alpha) and those whose objective is capital deployment.

The headlines are noisy. The reality is precise.

Let's be Clear: BDCs are Not the Problem

In recent news stories, financial journalists have been quick to point fingers at publicly traded BDCs, citing price declines, volatility, and negative total returns. That framing is incomplete – and in many cases, incorrect.

BDCs are a fund structure, not an investment strategy.

They can be well run or poorly run. Disciplined or undisciplined. Conservative or reckless.

What is failing today is not the structure. What is failing is credit discipline.

That distinction matters – because blaming the structure obscures the real lesson investors need to internalize.

The Real Divide: Beta Managers vs. Alpha Managers

Private credit has reached scale.

With approximately $3 trillion in assets under management, the private credit market has continued to evolve from a niche, relationship-driven ecosystem to a highly competitive capital market.

In Today’s Environment, Managers Fall into Two Very Different Camps:

Beta Players

These are capital deployers. They are characterized by:

- Returns that are driven primarily by exposure to floating rates

- Heavy reliance on scale, leverage, and transaction velocity

- Increasing use of covenant-lite documentation

- Frequent participation in dividend recaps and concentrated sponsor liquidity events, thereby shifting equity risk onto credit providers

- High pressure – and financial incentive – to deploy capital regardless of structure or terms

- Acceptance of increased risk to achieve competitive yields

Alpha Players

These are credit investors that focus on matching the amount of capital they raise to only the best underwriting opportunities. They are characterized by:

- Discipline on maintaining appropriate pricing, thereby avoiding compression of yields

- Willingness — and ability — to walk away from riskier deals

- Emphasis on first-lien, senior secured positions

- Adherence to strong maintenance covenants

- Not overly concentrated in underwriting to a few equity sponsors

- Avoidance of large, syndicated deals

Managers focused on selection, structuring, and discipline seek to generate returns through these characteristics rather than through deployment velocity or market beta exposure. The difference in approach becomes more visible during periods of market stress.

This is the fault line now running through private credit.

What We Are Seeing Now Is Exactly What We Expected

As base rates normalize and spreads remain compressed, structural weaknesses are being exposed.

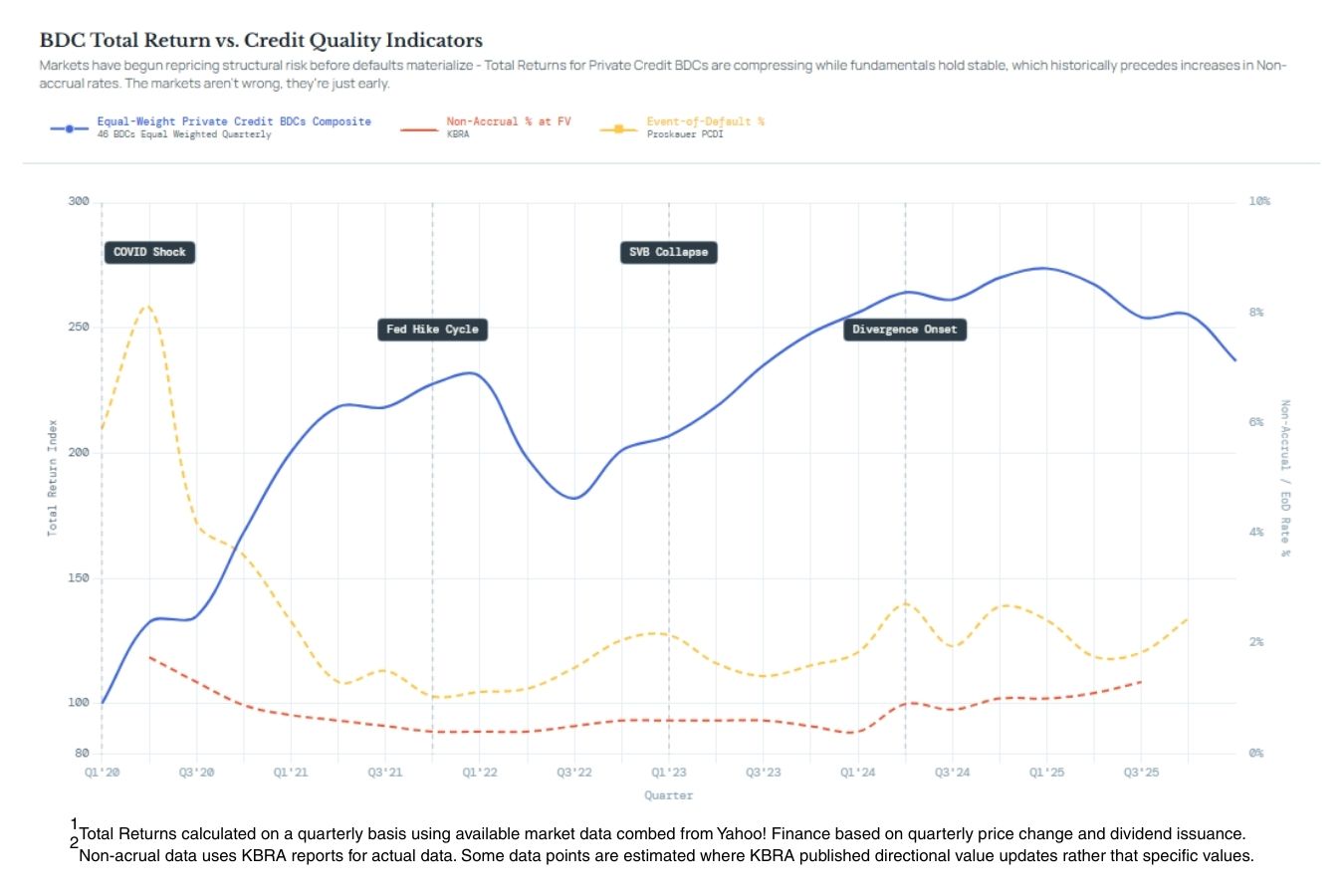

Importantly, this is happening despite relatively stable default data:

- Private credit default rates remain historically low

- BDC non‑accruals are contained

- Credit losses are not yet widespread

And yet, many publicly traded credit vehicles are down sharply. The table below shows a selection of publicly traded, private credit BDCs that have experienced selloffs in the last few quarters.

Why are we seeing this?

Because markets are repricing underlying risk factors, not realized losses.

Liquidity-sensitive vehicles, covenant-lite portfolios, and leveraged strategies are being discounted before defaults materialize — precisely because investors understand what happens next when discipline disappears. This is what markets do – they start to reprice risk before calamity hits. And investors would be wise to take note.

Structural Substitution Is the Silent Risk

To maintain headline yields in a competitive environment, many managers have turned to what institutional allocators now call “structural substitution”:

- Higher borrower leverage

- Weaker covenant packages

- Increased fund-level leverage

- Hidden refinancing risk

- Reduced lender control in stress scenarios

These are not marginal changes. They represent a reallocation of risk from equity sponsors to creditors — often without adequate compensation.

Returns that appear attractive on paper are, in reality, payment for assuming tail risk, not evidence of superior credit skill. That distinction is becoming impossible to ignore.

Scale Has Become a Constraint, Not an Advantage

The most overlooked dynamic in private credit today is scale pressure.

Managers overseeing tens of billions of dollars must deploy enormous amounts of capital every year — regardless of market conditions. At that size, lower-middle-market, covenant-heavy, bespoke lending becomes operationally difficult.

So, capital migrates upmarket to:

- Larger deals

- More competition

- Financial engineering

- Overlapping exposures

This is not theory. It is actually happening, and it is measurable when conducting diligence on private credit funds.

And it explains why size and brand are no longer reliable proxies for credit quality.

What Real Private Credit Alpha Looks Like

In this environment, alpha is not abstract. It is structural and observable.

It maintains:

- True seniority — first-lien, senior secured positioning lien

- Covenant protection — enforceable maintenance covenants

- Sponsor alignment — equity capital behind the borrower

- Appropriate use of funds — financing of CapEx, working capital, accretive M&A, NOT funding of indefinite operating losses and broken business models

- Refusal capacity — the ability to say no when terms deteriorate

Managers who preserve these characteristics are not insulated from volatility — but they are insulated from structural decay. That difference will compound over time.

This environment clarifies which returns are earned through underwriting and which are manufactured through leverage, weaker structure, and deployment momentum.

Periods like this clarify which returns are earned through underwriting and which are manufactured through leverage, weaker structure, and deployment momentum.

Private credit is not broken. It is being sorted.

And investors who understand the difference between fund structure and credit behavior and between headline yield and real risk will be positioned very differently when this cycle turns.

Historical market cycles have tended to favor discipline over deployment momentum, though past patterns do not guarantee future outcomes. Market conditions and investor preferences can shift based on numerous unpredictable factors. We believe this is precisely the environment where informed investors can build durable exposure by prioritizing credit discipline over scale and underwriting advantage over manufactured yield.

IMPORTANT DISCLOSURES This article is provided for informational and educational purposes only and does not constitute investment advice, a recommendation, or an offer or solicitation to buy or sell any securities or investment products. The views expressed are those of the author as of the publication date and may change based on market conditions and other factors. The information presented is based on publicly available data and the author's analysis. BIP Capital makes no representations as to the accuracy or completeness of third-party data presented. Performance data shown represents publicly traded securities and does not reflect the performance of any BIP Capital fund or separately managed account. Past performance is not indicative of future results. All investments involve risk, including the potential loss of principal. Private credit investments involve specific risks, including illiquidity, lack of transparency, use of leverage, and reliance on manager skill. The comparison between different investment approaches is for illustrative purposes only and does not represent an evaluation of any specific fund or manager. Different market conditions may favor different investment approaches. This article should not be relied upon as the sole basis for any investment decision. Investors should consult with their financial, tax, and legal advisors before making any investment.