How AI is forcing the market to rethink what every business is worth — and why that is both a warning and an opportunity

The entire market is in the middle of a very uncomfortable argument about what value means in a world where artificial intelligence can do in seconds what used to take a team of people a month.

The result is something we have never seen before: a simultaneous repricing of businesses across nearly every sector, driven not by a recession, a credit crisis, or a geopolitical shock — but by a single, relentless question that investors are asking about every company they own.

Is this business more durable because of AI, or less?

If you are trying to make sense of the market right now, that question is the Rosetta Stone. Everything else is noise.

The P/E ratio: a quick primer

For anyone who needs a quick refresher: a Price-to-Earnings (P/E) ratio is simply what investors are willing to pay for each dollar of a company's earnings. If a stock trades at 40x earnings, investors are paying $40 for every $1 of annual profit the business generates. Think of it like buying a rental property: the higher the price you are willing to pay relative to the rent it generates, the more confident you are that the rent is going to keep growing — or that the building will be worth a lot more in the future. Cut that confidence in half, and the price you are willing to pay drops accordingly, even if the rent itself has not changed at all yet.

That is exactly what is happening across the technology sector right now, with SaaS companies bearing the brunt of it. And unlike a traditional market correction, this repricing is not uniform. It is surgical. The market is distinguishing, with increasing precision, between companies that AI will disrupt and companies that AI will amplify.

The SaaS sector takes the first hit

Software-as-a-Service was the darling of equity markets (public and private) for the last 25 years. Investors were willing to pay 50x, 80x, even 100x earnings — or revenue, since many of these companies had no earnings at all — because the growth rates seemed almost gravitational. Every company in the world was becoming a software company. SaaS businesses had recurring revenue, sticky customers, and high gross margins. What was not to love?

Then two things happened. Interest rates rose, which made future earnings worth less in today's dollars. And then came the bigger disruption: AI began demonstrating that it could perform many of the tasks that SaaS tools were charging per seat to enable. As Klarna announced in 2025 that it had replaced Salesforce and Workday entirely with AI automation — and that its AI assistant was handling two-thirds of all customer service interactions — investors started asking hard questions about every SaaS business model.

"We are looking at a lot of software names that are seen as companies that may well be disrupted when we start to see the advancement of artificial intelligence. We are seeing a lot of software companies across the spectrum get hit." — Art Hogan, Chief Market Strategist, B. Riley Wealth

The result? The IGV ETF, which tracks North American software, fell nearly 28% from its September 2025 peak by early 2026. The sector's forward P/E collapsed from approximately 35x at the end of 2025 to roughly 20x — back to levels not seen since 2014. To put that in plain terms: the market cut its confidence in the earnings durability of software businesses nearly in half, in a matter of months.

Seven SaaS names that have seen multiple compression

Below is a look at seven leading SaaS companies where the market has meaningfully reduced the premium it is willing to pay. The "Peak Multiple" reflects the approximate forward P/E or EV/Revenue multiple at or near the November 2021 peak, and the "Current Multiple" reflects approximate levels as of early 2026.

Reading between the lines: what these numbers actually mean

Let me give you a useful mental model. If a business was trading at 100x earnings and it is now trading at 50x earnings, two very different stories are possible. The pessimistic story is that the market believes future earnings will be lower — either because revenue growth has slowed, because AI is eroding pricing power, or because a competitor with zero marginal cost can do the same job. That is a real earnings impairment, and the multiple compression is warranted.

But here is the other story, and it is just as plausible: the business in question has actually embraced AI, used it to improve its own margins, and is now more efficient, more scalable, and more durable than before. In that case, the same 50x multiple represents a buying opportunity — the market has punished the whole sector without distinguishing the adapters from the disrupted.

Take Snowflake. On the surface, a collapse from 200x EV/Revenue looks catastrophic. But dig into the business. Snowflake's partnership with Anthropic to bring Claude models directly onto its data platform is a strategic move. Their remaining performance obligations surged 37% to $7.88 billion in late 2025, meaning future contracted revenue is growing rapidly. The real debate is whether the market is discounting the stock for the right reason (near-term margin compression from heavy AI investment) or the wrong reason (assuming the business is being disrupted). Those are two very different bets.

UiPath is another fascinating case. Robotic Process Automation was supposed to be made obsolete by AI agents. Instead, UiPath's Q3 FY2026 revenue grew 16% year-over-year, and the company struck deep partnerships with both OpenAI and Nvidia — positioning its platform as the orchestration layer for agentic AI across claims processing, financial workflows, and enterprise operations.

Salesforce is the most-watched bellwether. The stock has faced its worst stretch since 2004. But Salesforce's Agentforce AI product saw annual revenue more than triple in a single year to exceed half a billion dollars, and the company raised full-year FY2026 revenue guidance to $41.45–$41.55 billion. The question is not whether Salesforce will survive — it is whether a 27x forward P/E adequately prices in a business that is reinventing itself as an AI platform company.

The core mental model — Scenario A (Warranted compression): AI genuinely erodes the business model. Revenue durability is reduced. The lower multiple is correct. Scenario B (Mispriced opportunity): The company successfully leverages AI to improve margins, expand use cases, and deepen customer relationships. The lower multiple represents a discount to intrinsic value. The investor's job is to determine which scenario applies — and the market is currently pricing many names as Scenario A without doing the work to distinguish them.

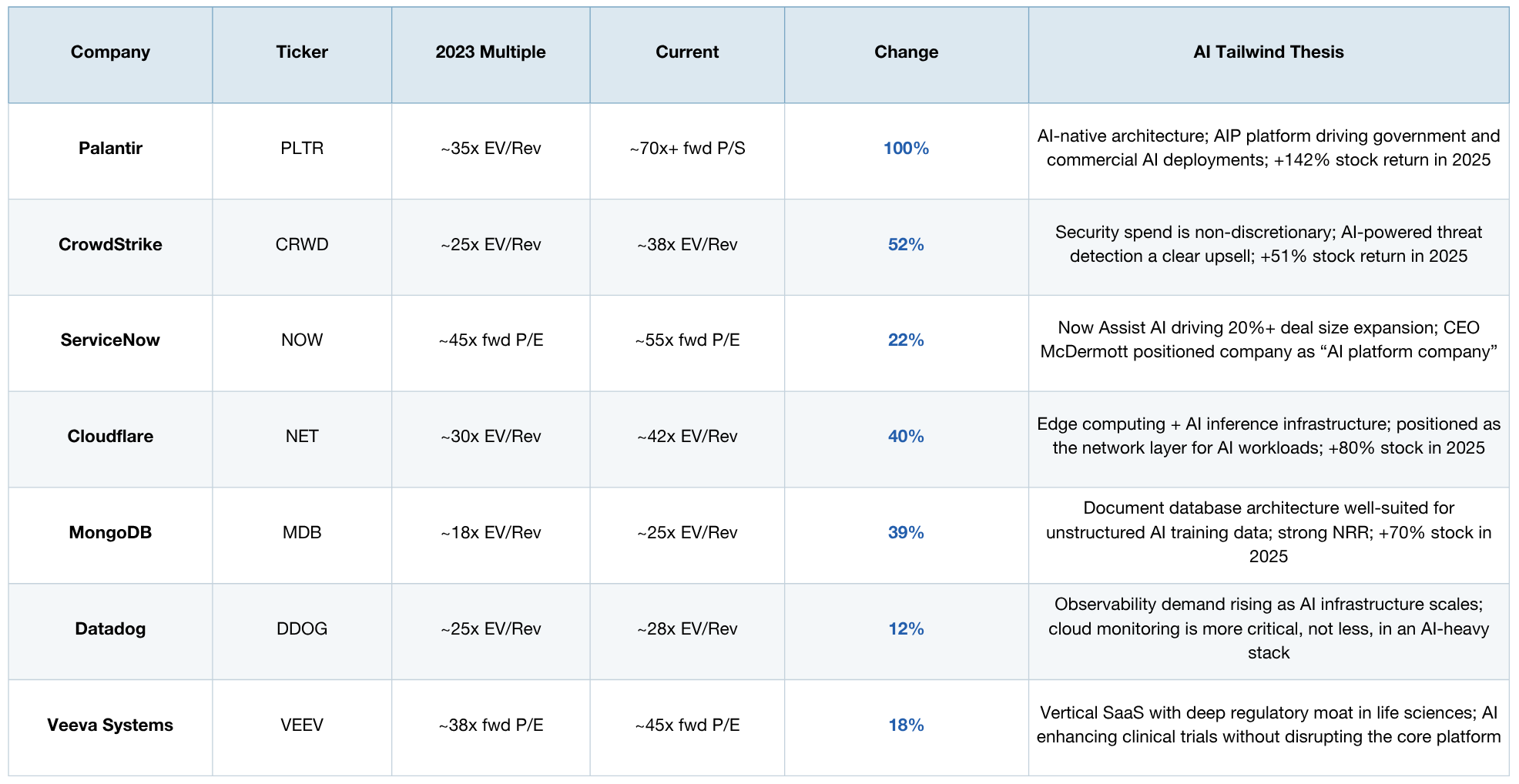

Seven SaaS names where multiples have expanded

Not all SaaS names are in the penalty box. A handful of companies have seen their multiples hold or expand — and the common thread is unmistakable: each has demonstrated that AI is a source of earnings growth, not a threat to it.

The pattern here is not subtle. Goldman Sachs' prime brokerage data showed net hedge fund exposure to software reaching its highest level since early 2024 — but concentrated almost entirely in AI-linked names. The market is not anti-software. It is anti-ambiguity.

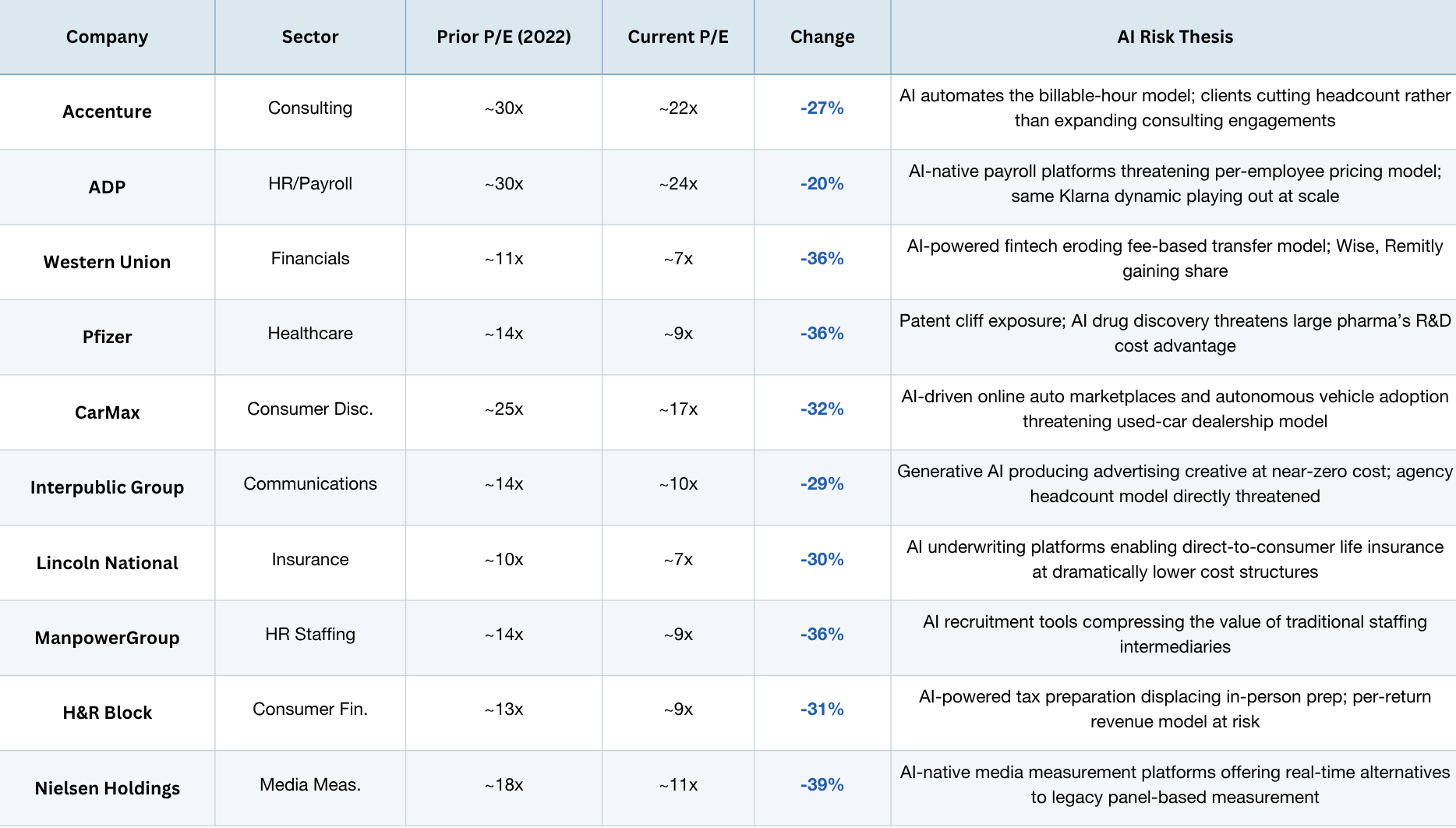

Beyond tech: ten S&P 500 names where AI is compressing multiples

The repricing is not confined to software. The "Great Rotation" underway in early 2026 reflects a broader recognition that AI disruption risk lives in every sector where human labor or routine cognitive work is the primary value driver.

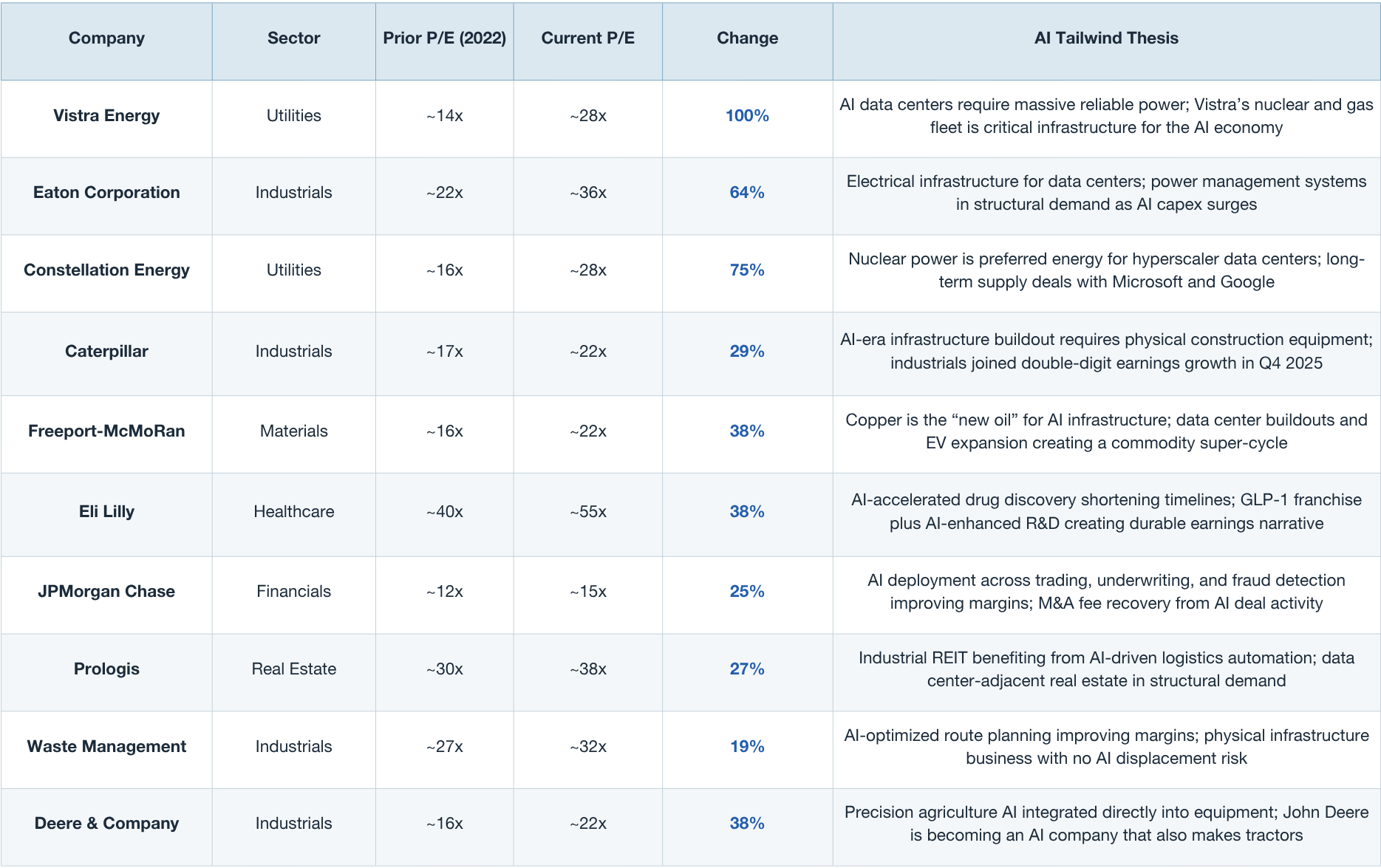

Ten S&P 500 names outside tech where multiples are expanding

These are businesses whose earnings are becoming more durable in an AI world — either because they supply the physical infrastructure AI requires, benefit from AI-driven productivity, or operate in sectors where human judgment and regulatory moats keep AI at bay.

"The AI trade in 2026 is likely to be defined by a deceleration in investment spending growth, a rise in AI adoption, and companies boosting efficiency through the use of AI — expanding the focus well beyond direct infrastructure beneficiaries." — Goldman Sachs Research, January 2026

What should you actually do with this information?

It is tempting to look at these tables and conclude that you should simply sell everything in the "compression" category and buy everything in the "expansion" category. But markets are not that simple, and neither is AI.

First, do not confuse multiple compression with business impairment. The market has painted a lot of businesses with the same AI-risk brush, and some of them are being punished for sins they have not committed. A SaaS company with deep workflow integration, proprietary data, and high switching costs is not the same as one selling generic tooling that an LLM can replace in an afternoon.

Second, pay attention to the "adapter vs. disrupted" distinction at every level of the portfolio — not just in tech. The consulting firms, staffing agencies, and insurance underwriters in the compression table above are not necessarily doomed. But they have to earn a higher multiple back by demonstrating that their business model survives contact with an AI-native competitor. Or, they have to cleverly combine AI-native solutions with existing value delivery models. The ones that do that work will be the contrarian opportunities of the decade. This is where we are focused at BIP Capital and at BIP Wealth.

Third, remember that physical scarcity is the ultimate moat in a digital world. You cannot train an AI model without electricity. You cannot run a data center without copper wiring and land. The market figured this out in 2025 and early 2026, and the multiple expansion in utilities, industrials, and materials reflects that insight. Whether those multiples are now fairly priced — or whether they have overshot — is the next question worth asking.

I have spent a lot of time in my career evaluating businesses at the intersection of technology and capital markets. The businesses that survive transformational technological shifts are rarely the ones that resist the change, and rarely the ones that get swept up in the hype. They are the ones that figure out how to make the new technology work for them — and that communicate that capability credibly to the market. The P/E ratio is just the market's running scorecard on how convincingly they are doing it.

The great repricing is not over. But for investors willing to do the work, it is one of the more interesting environments we have seen in years.

Questions worth asking yourself:

Are the managers you have selected prepared for the AI-Revolution? Have they stress-tested their holdings against an AI-native competitor entering their market? And for the businesses in their portfolio that are seeing multiple expansion — is the premium driven by genuine AI-enabled earnings durability, or just narrative momentum?

I would love to hear how you are thinking about this. And we are happy to share much deeper analytical insights on this topic with clients and prospective clients. Drop a comment, reach out directly, or share this with a colleague who is wrestling with the same questions. The best investment insights usually come from the conversations that follow pieces like this one.