In traditional private market funds, the J-curve describes the performance pattern in which reported returns are negative or flat in the early years of a fund’s life, then turn positive as investments mature and are realized. For advisory firms introducing private markets to clients, the J-curve is one of the most consequential concepts to understand — and one of the most important to communicate before the first quarterly statement arrives.

The advisory firm that has set client expectations before the first statement arrives is in a fundamentally different position than the one responding to a concerned client call six months after an allocation closes. That difference in outcome almost always traces back to a single conversation — one that either happened before the investment or did not.

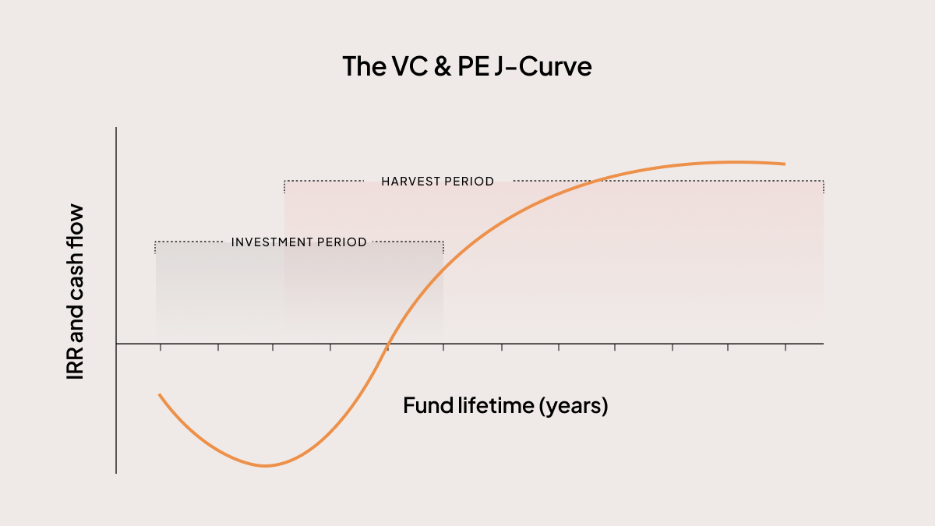

The J-Curve: A Structural Overview

The J-curve describes a performance pattern common to traditional closed-end private market funds: reported returns are negative in the early years before recovering and, eventually, generating meaningful appreciation. Plotted on a chart, the trajectory resembles the letter “J” — an initial decline followed by gradual recovery.

The J-curve is not a warning sign. It is the natural consequence of how traditional private funds are structured. Three core mechanics drive it.

Management Fees and Fund Expenses Arrive Before Deployment

A private fund begins incurring costs before it deploys a single dollar of capital. Management fees, legal expenses, audit costs, organizational expenses, and fund administration all begin immediately. Those costs are reflected in the fund’s net asset value before investments have had time to generate returns. For 2024 vintage buyout funds, mean management fee rates were approximately 1.74%; for growth equity funds, approximately 1.93%. On a $100M commitment, that represents $1.7–2M per year in costs before a single acquisition closes or a loan is originated.

The result: most funds begin their lives slightly below zero — not because something went wrong, but because the structural costs of running a fund precede the deployment of capital.

Capital Is Deployed Gradually Over the Investment Period

Private equity and credit funds invest capital over a multi-year investment period, typically three to five years, as managers source opportunities, complete due diligence, and negotiate terms. A fund six months old may have invested only a fraction of its committed capital. The portfolio has not yet had sufficient time to generate meaningful appreciation, and reported returns reflect that incomplete deployment.

Early Investments Are Typically Carried at Cost

In the early life of a fund, portfolio companies are typically carried at or near their original valuations. Meaningful appreciation is recognized only after a company has grown revenues, improved margins, completed accretive acquisitions, or approached a monetization event. Those developments take years, not quarters. The portfolio can be performing exactly as intended while reported returns remain flat or slightly negative — because the reporting reflects cost, not yet realized outcome.

The J-curve is not a flaw in private market fund structures. It is a feature of how many private market strategies create value over time.

How the J-Curve Differs Across Fund Structures

Not every private market vehicle experiences the J-curve the same way. The structural differences across fund types are significant — and understanding them is essential context for advisory firms evaluating how to introduce private markets across their client base.

Traditional Closed-End Private Equity and Venture Capital Funds

In traditional venture capital and private equity funds, the J-curve is often pronounced. Returns are frequently negative in years one and two, and performance may remain relatively flat in years three and four as capital continues to be deployed and portfolio companies mature. The most meaningful appreciation in these vehicles often occurs during years five through eight, with distributions arriving as companies are sold or taken public.

Buyout funds typically carry shallower, shorter curves because they invest in more mature businesses that generate cash flow earlier. Venture capital funds tend to carry a deeper, longer curve because early-stage companies require more time to reach the milestones that drive valuation recognition. The advisory firm’s role when evaluating traditional funds is both to assess client fit based on financial profile and long-term objectives, and to calibrate client expectations across the full arc of the investment period.

Evergreen Structures, BDCs, and Interval Funds

For advisory firms introducing private markets for the first time, evergreen structures can meaningfully reduce many of the behavioral challenges historically associated with traditional closed-end fund investing. Because new investors typically gain exposure to an already-functioning portfolio, much of the traditional J-curve is compressed or eliminated. Capital is generally deployed immediately into existing assets rather than accumulating during a multi-year investment period.

This dynamic is particularly evident in income-oriented private credit strategies. Many Business Development Companies and evergreen private credit vehicles begin generating income shortly after investment because investors are purchasing exposure to a portfolio of already-originated loans rather than waiting for a manager to build one.

Evergreen structures and BDCs also reduce several operational frictions that historically limited adoption: no capital call management, lower investment minimums, NAV-based pricing, and always-open subscription windows. These structural features reduce the barriers that prevent advisory firms from having the allocation conversation in the first place.

Why the J-Curve Matters Now

For most of private markets’ institutional history, the J-curve was primarily a concern for pension funds, endowments, and family offices — sophisticated allocators who built portfolios around long-term capital commitments and understood the tradeoff between near-term reported performance and long-term value creation.

As evergreen funds, BDCs, interval funds, and other investor-friendly structures have expanded access to private markets, advisory firms are increasingly introducing these strategies to clients who may have spent decades investing exclusively in public securities. Those clients often bring public-market expectations with them — including the expectation that every investment should produce visible, immediately reportable results.

That shift makes client expectation-setting more critical than ever. Whether an advisory firm is evaluating a traditional closed-end private equity fund, an evergreen structure, a BDC, or an interval fund, understanding how performance is likely to develop over the life of the investment is essential to building durable client confidence. Behavioral errors — redeeming early, losing conviction, withdrawing capital at the wrong moment — are among the most common causes of underperformance in private market allocations, and most of them are preventable through deliberate, structured communication before the allocation is made.

Advisory firms that understand the J-curve, and communicate it clearly before the first statement arrives, are better positioned to build the kind of client relationships that withstand the inevitable early-period volatility in reported returns — and to build private market programs that compound over time.

Frequently Asked Questions About the J-Curve

Is the J-curve normal?

Yes. Early negative or flat returns are a structural feature of traditional closed-end private equity and venture capital funds, not a signal that something has gone wrong. The mechanics are predictable: management fees begin accruing before the first investment closes, capital deploys gradually over a multi-year investment period, and early-stage portfolio companies are typically carried near cost until they reach the milestones that drive valuation recognition. The depth and duration of the curve vary by strategy and manager, but the pattern itself is a known and anticipated feature of the asset class.

How long does the J-curve last?

Duration varies meaningfully by strategy. For buyout funds, the curve is typically shallower — meaningful cash flow from mature portfolio companies can emerge within two to three years. Venture capital funds carry a longer curve, often extending through years four or five, because early-stage companies require more time to reach the milestones that drive valuation recognition. Evergreen structures compress or eliminate the curve entirely by providing immediate exposure to an established portfolio.

Do evergreen funds have a J-curve?

Many evergreen structures experience a reduced or compressed J-curve because investors typically gain immediate exposure to an already-invested portfolio. The degree of compression depends on the specific structure and the maturity of the underlying portfolio at the time of subscription.

Is a negative return during the first year a problem?

Not necessarily. In a traditional closed-end fund, the more relevant question at that stage is whether the manager is deploying capital on the timeline committed to and building the portfolio as described in the offering documents. Early interim performance reflects fees and conservative early valuations — not terminal outcome. For closed-end funds, terminal value is the appropriate scorecard, not interim NAV reported during the deployment period.